Are you tired of the daily grind and dreaming of a life of leisure? Early retirement might seem like a pipe dream, but it’s achievable with the right planning and strategy. Financial freedom allows you to escape the 9-to-5, pursue your passions, and enjoy life on your own terms. This article will guide you through the essential steps of early retirement planning, helping you take control of your future and secure your financial independence.

Achieving financial freedom through early retirement requires a proactive approach. It involves saving, investing, and making strategic choices about your finances. By understanding the key principles of early retirement planning, you can build a solid foundation for a comfortable and fulfilling life beyond traditional retirement age.

Defining Your Early Retirement Goals and Vision

Early retirement is a dream for many, but it’s important to have a clear vision of what that dream looks like before you can achieve it. What does early retirement mean to you? Is it about financial freedom, spending more time with loved ones, or pursuing a passion project? Once you understand your goals, you can start creating a plan to make them a reality.

First, consider your financial goals. How much money will you need to live comfortably in retirement? How long do you want to retire for? What are your spending habits? Once you have a good understanding of your financial needs, you can start creating a budget and saving plan.

Next, think about your lifestyle goals. What do you want to do with your time in retirement? Do you want to travel the world, start a business, or simply relax and enjoy your hobbies? Be specific about your goals and write them down so you can refer to them as you plan your retirement.

Finally, it’s important to have a vision for your retirement. Imagine yourself living the life you desire and write down what it looks like. Do you see yourself living in a warm climate, spending time with your family, or exploring new cultures? The more detailed your vision, the more motivated you’ll be to work towards it.

Defining your early retirement goals and vision is the first step to achieving your dream. It allows you to create a plan that is tailored to your individual needs and desires. With a clear understanding of what you want, you can start taking steps to make early retirement a reality.

The Benefits of Early Retirement Planning

Planning for retirement early on has numerous benefits. It allows you to take control of your financial future, reduce stress, and enjoy a more fulfilling life. Here are some of the key advantages:

Financial Security

Early retirement planning allows you to start saving early, giving your investments more time to grow through compounding. This means you can accumulate a larger nest egg, providing financial security during your retirement years. You’ll have the flexibility to pursue your passions without worrying about money, making retirement truly enjoyable.

Flexibility and Choices

Retirement planning allows you to explore different options and make informed decisions about your future. You can choose to retire earlier than planned, pursue part-time work, or take on new ventures without financial constraints. This flexibility empowers you to design your retirement according to your goals and aspirations.

Reduced Stress

Knowing that your finances are secure can significantly reduce stress levels. You’ll have peace of mind knowing that you can comfortably afford your living expenses, healthcare, and other essential needs during retirement. This financial security contributes to a more relaxed and enjoyable life.

Enhanced Health and Well-being

Early retirement planning can positively impact your health and well-being. Studies have shown that people who retire early often enjoy better physical and mental health. They have more time for leisure activities, stress reduction, and maintaining a healthy lifestyle.

Time for Pursuits and Passions

Retirement is a time for pursuing passions and exploring new interests. Early planning allows you to devote more time to hobbies, travel, volunteer work, or spending quality time with loved ones. This newfound freedom can lead to a more fulfilling and meaningful life.

In conclusion, early retirement planning offers numerous benefits, including financial security, flexibility, reduced stress, enhanced health, and time for personal pursuits. By starting early and making informed financial decisions, you can create a secure and enjoyable retirement that aligns with your goals and aspirations.

Calculating Your Retirement Expenses and Income Needs

Retirement is a significant milestone in life, and it’s crucial to plan financially for this phase. One of the most important aspects of retirement planning is determining your retirement expenses and the income you’ll need to cover them. This article will guide you through the process of calculating your retirement expenses and income needs, ensuring you have a comfortable and financially secure retirement.

Estimating Retirement Expenses

The first step is to estimate your retirement expenses. This involves considering your current spending habits and projecting them into the future, taking into account factors such as inflation and changes in your lifestyle. You can start by analyzing your current monthly expenses and categorizing them into different areas, such as:

- Housing

- Food

- Transportation

- Healthcare

- Entertainment

- Travel

- Other expenses

Once you have a clear understanding of your current expenses, you can adjust them for inflation and lifestyle changes. For instance, you may need to adjust your housing expenses if you plan to downsize or relocate. Similarly, healthcare expenses may increase as you age. You can use online inflation calculators to estimate the impact of inflation on your expenses over time.

Considering Lifestyle Changes in Retirement

Retirement often brings about significant lifestyle changes. Some people may choose to travel more, pursue hobbies, or spend more time with family and friends. These activities can impact your expenses. Consider whether you plan to:

- Travel frequently

- Take up new hobbies or activities

- Move to a different location

- Provide financial support to family members

Based on your anticipated lifestyle changes, you can adjust your expense estimates accordingly.

Calculating Retirement Income Needs

After estimating your retirement expenses, you can calculate your income needs. This involves determining the amount of income you’ll require to cover your expenses comfortably. You can use the following formula:

Retirement Income Needs = Annual Retirement Expenses / (Annual Rate of Return on Investments)

For example, if your annual retirement expenses are $50,000 and you expect an average annual rate of return on your investments of 5%, your retirement income needs would be $1 million ($50,000 / 0.05 = $1,000,000).

Seeking Professional Advice

It’s important to note that these calculations are just estimates, and your actual retirement expenses and income needs may vary. It’s highly recommended to seek professional financial advice from a qualified financial advisor. They can help you assess your financial situation, develop a comprehensive retirement plan, and ensure you have enough savings and income to meet your retirement goals.

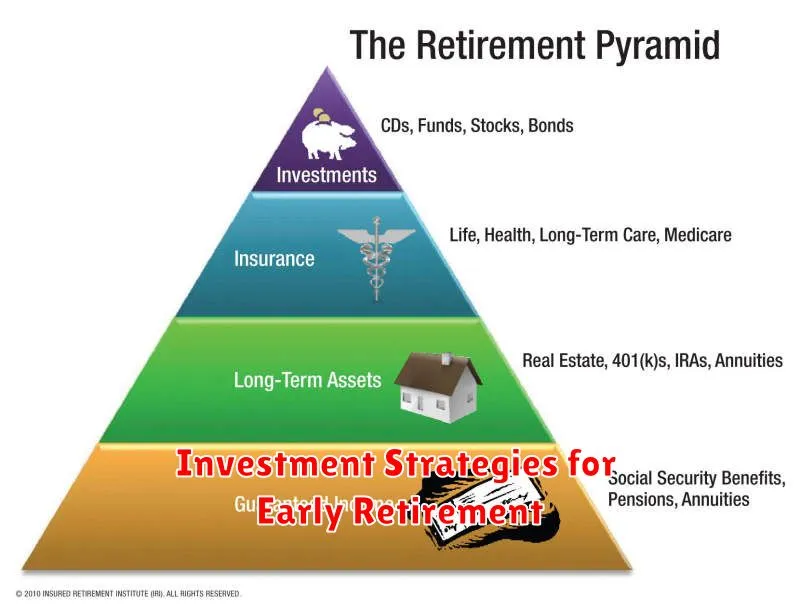

Investment Strategies for Early Retirement

Retiring early is a dream for many, but it requires careful planning and a solid investment strategy. Achieving financial independence before the traditional retirement age demands a proactive approach to saving, investing, and managing your money.

1. Start Early and Save Aggressively

The earlier you start investing, the more time your money has to grow. Compound interest is your greatest ally in early retirement, as it allows your investments to generate returns on both the principal amount and the accumulated interest. Aim to save as much as possible, ideally 15-20% of your income, and prioritize high-growth investments.

2. Embrace a Diversified Portfolio

Don’t put all your eggs in one basket. Diversifying your investments across different asset classes, such as stocks, bonds, real estate, and commodities, helps mitigate risk. A diversified portfolio balances potential gains with risk management, ensuring your investments are not overly exposed to any single market fluctuation.

3. Explore High-Growth Investments

To achieve early retirement, you need investments that can potentially generate substantial returns. Consider investing in growth stocks, real estate, or alternative assets like private equity or venture capital. These investments carry higher risk, but they also offer the potential for significant capital appreciation. Remember to carefully research and understand the risks before investing.

4. Minimize Expenses and Live Below Your Means

To reach early retirement, you must reduce your expenses to a manageable level. Identify areas where you can cut back on spending and create a budget that reflects your financial goals. Consider downsizing your home, simplifying your lifestyle, and prioritizing experiences over material possessions.

5. Seek Professional Guidance

Working with a financial advisor can provide valuable insights and customized strategies for early retirement. They can help you assess your financial situation, set realistic goals, and develop a personalized investment plan that aligns with your risk tolerance and time horizon. A qualified advisor can also provide guidance on tax optimization and estate planning.

6. Embrace a Long-Term Perspective

Early retirement is not a sprint; it’s a marathon. The market will experience ups and downs, and there will be times when your investments may not perform as expected. Stay focused on your long-term goals and avoid making impulsive decisions based on short-term market fluctuations. Patience and discipline are crucial for achieving your retirement aspirations.

Investing for early retirement requires a well-defined strategy and a commitment to disciplined saving and investing. By starting early, diversifying your portfolio, and making smart financial decisions, you can increase your chances of achieving financial freedom and retiring on your own terms.

Maximizing Retirement Savings Through Tax-Advantaged Accounts

Retirement planning is a crucial aspect of financial well-being, and one of the most effective strategies for securing a comfortable future is maximizing savings through tax-advantaged accounts. These accounts offer significant benefits that can help you accumulate wealth and potentially reduce your tax burden.

Types of Tax-Advantaged Retirement Accounts:

There are several types of tax-advantaged retirement accounts available, each with its own unique features and benefits. Here are two of the most common:

Traditional IRAs

Traditional Individual Retirement Accounts (IRAs) allow pre-tax contributions to grow tax-deferred. This means you won’t pay taxes on the earnings until you withdraw them in retirement. Contributions may also be tax-deductible, potentially lowering your current tax bill.

Roth IRAs

Roth IRAs, on the other hand, involve after-tax contributions. While you don’t receive a tax deduction upfront, qualified withdrawals in retirement are tax-free. This can be advantageous if you anticipate being in a higher tax bracket in retirement.

Benefits of Tax-Advantaged Retirement Accounts:

Tax-advantaged retirement accounts offer several compelling benefits, including:

- Tax Savings: By allowing for pre-tax contributions or tax-free withdrawals, these accounts can significantly reduce your tax burden throughout your life.

- Compounding Growth: Tax-deferred growth allows your investments to compound faster, as you are not paying taxes on earnings along the way.

- Protection from Taxes: In most cases, withdrawals from retirement accounts are subject to taxes, but tax-advantaged accounts offer protection from taxes on your earnings.

- Flexibility: Many retirement accounts offer flexibility in terms of contribution amounts, investment options, and withdrawal rules.

Maximizing Your Savings:

To maximize your retirement savings through tax-advantaged accounts, consider these tips:

- Contribute as much as possible: Take advantage of the annual contribution limits for your chosen account.

- Start early: The earlier you start saving, the more time your investments have to grow.

- Choose investments wisely: Diversify your portfolio to manage risk and potentially maximize returns.

- Review your strategy regularly: As your financial situation evolves, consider adjusting your retirement savings plan accordingly.

Conclusion:

Tax-advantaged retirement accounts are essential tools for building a secure financial future. By understanding the benefits and maximizing your contributions, you can set yourself up for a comfortable and fulfilling retirement.

Creating Multiple Streams of Passive Income

Passive income is a great way to supplement your regular income or even replace it entirely. It is money that you earn without actively working for it. There are many different ways to generate passive income, and it is important to find a strategy that works for you.

One of the most popular ways to create passive income is through investing. There are many different investment options available, such as stocks, bonds, real estate, and more. The key is to choose investments that are aligned with your risk tolerance and financial goals.

Another common method is to create and sell digital products. This could include ebooks, online courses, templates, or even software. Once you create the product, you can sell it online and continue to earn money from it, even while you are sleeping.

Affiliate marketing is also a popular way to generate passive income. You partner with businesses and promote their products or services on your website or social media channels. When someone clicks on your link and makes a purchase, you earn a commission.

If you are creative, you could also consider creating and selling physical products. This could include handmade jewelry, clothing, or artwork. You can sell these products online through platforms like Etsy or Shopify.

Renting out a property is a great way to generate passive income from real estate. This could be your primary residence, a vacation home, or even a storage unit. You can rent out the property on a short-term or long-term basis.

No matter which method you choose, it’s important to be patient and persistent. It takes time to build up a passive income stream, but it can be incredibly rewarding in the long run. Remember to stay consistent with your efforts and keep learning and adapting as the market evolves.

Managing Healthcare Costs in Early Retirement

Retiring early can be a dream come true, but it’s important to consider the financial implications, especially when it comes to healthcare. While you may have years to go before you’re eligible for Medicare, navigating healthcare costs during this period requires careful planning.

Here’s a breakdown of strategies to manage healthcare expenses in early retirement:

1. Explore Your Coverage Options

Before you retire, research your available healthcare options. Consider:

- COBRA: This allows you to continue your employer-sponsored health insurance for a limited time, but premiums can be high.

- Individual Health Insurance Marketplace: Explore plans through the Affordable Care Act (ACA), where you may qualify for subsidies based on your income.

- Medicare: If you’re eligible for Medicare due to a disability or certain conditions, you can enroll early.

2. Maximize Your Savings

Build a robust healthcare savings strategy to cover out-of-pocket expenses:

- Health Savings Account (HSA): An HSA is a tax-advantaged account for healthcare costs. It’s ideal for those with a high-deductible health plan. Contributions grow tax-free and withdrawals are tax-free for qualified medical expenses.

- Flexible Spending Account (FSA): An FSA allows you to set aside pre-tax money to pay for eligible medical expenses. However, funds may be forfeited if unused by year’s end.

3. Consider a Part-Time Job

Maintaining some form of employment can offer you continued health insurance coverage, as well as additional income. Consider a part-time position that provides health benefits.

4. Be Proactive with Your Health

Preventive care can help lower healthcare costs in the long run. Stay up-to-date with checkups, screenings, and vaccinations.

5. Negotiate and Shop Around

Don’t hesitate to negotiate prices with healthcare providers. Research different options and compare costs for treatments, medications, and facilities.

6. Embrace a Healthy Lifestyle

A healthy lifestyle can significantly reduce healthcare costs. Eat nutritious foods, exercise regularly, and manage stress to maintain overall well-being.

By planning ahead and making informed decisions, you can effectively manage healthcare costs during your early retirement years. Enjoy your newfound freedom while feeling secure about your financial health.

Factors to Consider When Choosing an Early Retirement Date

Retirement is a significant milestone in life, and deciding when to retire is a personal decision that requires careful consideration. While some individuals eagerly anticipate the day they can hang up their hats and enjoy leisure, others may find it difficult to give up the structure and purpose that work provides. If you’re considering early retirement, there are several key factors to weigh before making this life-altering decision.

Financial Security

Financial security is arguably the most crucial factor when deciding on an early retirement date. You need to make sure you have enough saved to cover your living expenses, healthcare costs, and any other anticipated expenditures. It’s essential to have a clear understanding of your financial situation, including your income, expenses, and savings. Consider consulting with a financial advisor to create a comprehensive retirement plan that outlines your financial needs and potential sources of income.

Health and Well-being

Your health and well-being play a significant role in determining your readiness for retirement. Evaluate your current health status, considering any potential health issues that could impact your retirement years. It’s important to consider how you plan to stay active and engaged in your later years. If you’re passionate about travel, exploring new hobbies, or volunteering, factor these activities into your retirement plans.

Personal Goals and Interests

Retirement is an opportunity to pursue personal goals and interests that may have been put on hold during your working years. Consider what brings you joy and fulfillment and how you plan to spend your time in retirement. Do you dream of traveling the world, writing a novel, starting a business, or spending more time with family and friends? Reflect on your passions and create a plan to bring them to life during retirement.

Social Connections

Retirement can sometimes lead to a decrease in social interaction, especially if you derive a significant portion of your social connections from your workplace. Think about how you will maintain social connections in retirement. Consider joining social groups, volunteering in your community, or connecting with former colleagues. Maintaining a robust social life is essential for your mental and emotional well-being.

Legacy and Purpose

Some individuals find purpose and meaning in their careers and may struggle to transition to a life without work. If this is the case, consider how you plan to find purpose and meaning in retirement. Perhaps you’d like to share your skills and knowledge with others through mentorship or volunteering. Or maybe you’d like to leave a lasting legacy by pursuing a passion project or starting a charitable foundation.

Choosing an early retirement date is a significant decision that should not be taken lightly. By carefully considering these factors, you can make an informed choice that aligns with your individual circumstances and goals.

Adjusting Your Plan Over Time and Staying on Track

It’s important to remember that plans are not set in stone. As your life changes and new opportunities arise, you may need to adjust your plan to accommodate these changes. Don’t be afraid to make adjustments as needed, as long as you are still working towards your overall goals.

Here are some tips for adjusting your plan over time:

- Review your plan regularly: It’s a good idea to review your plan at least once a year, or even more often if your circumstances change significantly. This will help you to ensure that your plan is still relevant and that you are still on track to achieve your goals.

- Be flexible: Be willing to make adjustments to your plan as needed. Don’t be afraid to change your goals or strategies if you find that they are not working for you. Flexibility is key to staying on track.

- Track your progress: Regularly track your progress towards your goals. This will help you to identify areas where you are succeeding and areas where you need to improve. This will help you to stay motivated and make necessary adjustments to your plan.

- Celebrate your successes: It’s important to celebrate your successes along the way. This will help you to stay motivated and keep moving forward.

Staying on track with your plan can be challenging, but it is essential for achieving your goals. By following these tips, you can adjust your plan over time and stay on track to achieve your dreams.

{kind=link}